India’s FMCG story has entered a new chapter. Despite margin pressures, one-off tax realignment and transient distribution disruptions, collections and consumption have surprised on the upside. Underneath the numbers — falling inflation, GST reform, rural traction and digital reach — a durable recovery is taking shape. This report traces that turnaround from multiple angles: macro, corporate, consumer behaviour, channel evolution and strategic priorities for businesses and investors

Executive summary (key takeaways)

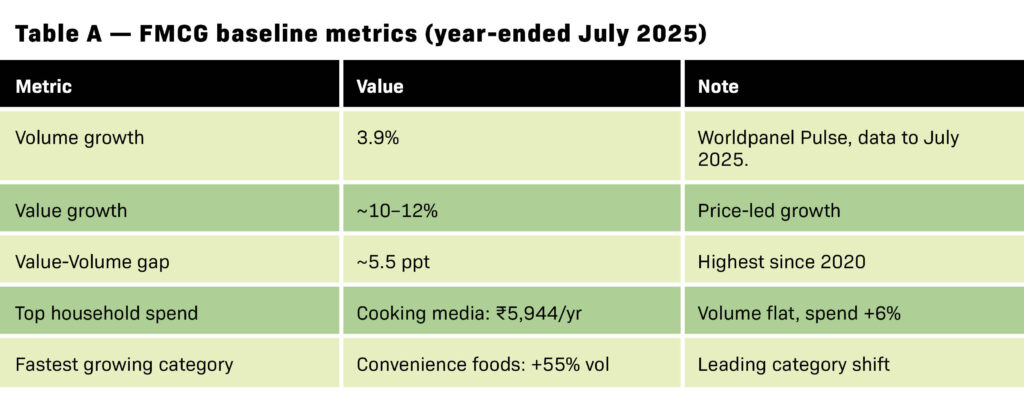

- Baseline weakness was real but short-lived: Worldpanel’s FMCG Pulse (data through July 2025) recorded a modest 3.9% volume growth baseline. That snapshot accurately captured consumer restraint but not the rapid policy pivot and inflation easing that followed.

- GST 2.0 is a structural catalyst: The September 2025 slab rationalisation (effective 22 Sep 2025) moved many mass-consumption FMCG items into a lower (5%) slab, creating perceptible household savings when aggregated over a main basket. This is a multi-quarter demand lever.

- Inflation fell sharply: Official CPI for September 2025 was ~1.54% YoY, restoring purchasing power and enabling discretionary refresh. This materially improves the starting point for real volume growth.

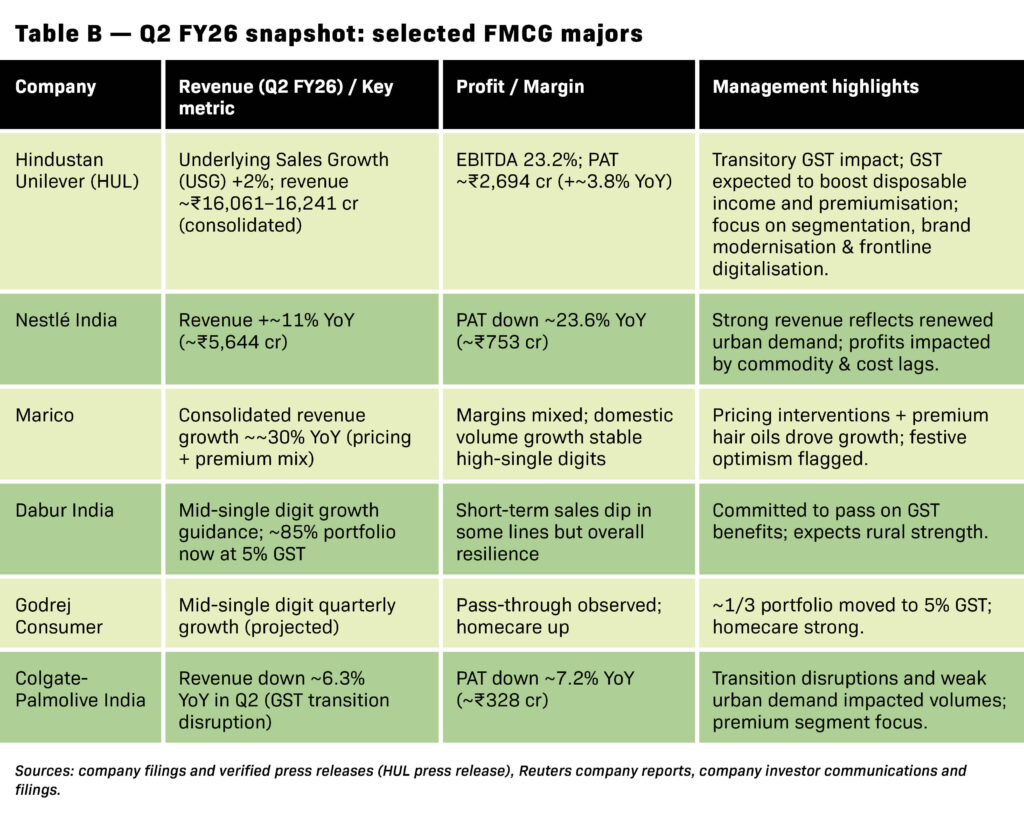

- Corporate evidence of recovery (Q2 FY26): Large firms show top-line improvement but margin pressure in Q2 as GST transition and commodity lagged. HUL reported Underlying Sales Growth (USG) +2% and EBITDA 23.2%; Nestlé India revenue rose ~11% while PAT declined; Marico posted ~30% consolidated revenue growth and Dabur highlighted ~85% of its portfolio moving to 5% GST. These results validate volume traction and the trade-transition story.

- Channel & geography fuel: Tier-II/III and rural markets are leading growth, and quick-commerce + e-commerce continue to amplify reach — creating a durable, multi-channel growth engine.

- Outlook: Base case FY26 volumes 5–6% (with upside to 7–8% if pass-through is full and commodity costs soften). Profitability likely to improve as volumes scale and commodity pressures ease.

I. The starting point — what the Pulse baseline taught us

Worldpanel’s October 2025 FMCG Pulse (data through July 2025) is the most recent, detailed household-panel view preceding the GST reform and the CPI drop. It documented:

- Volume growth ~3.9% (year ending July 2025), down from 5.4% a year prior. Value growth diverged sharply (~10–12%), yielding a value–volume gap of ~5.5 percentage points — the largest recent divergence and a clear symptom of input-cost inflation and price pass-through.

- Category patterns: convenience foods surged in volume (+55%), while staples (cooking media) held high spend per household (~Rs. 5,944/year) but flat volumes; health & pain relief categories held premium pricing power and stable volumes.

- Consumer sentiment: households overwhelmingly prioritized essentials, reduced discretionary purchases, and tried low-cost alternatives. The “main basket” concept emerged as decisive — savings matter most when aggregated across many items.

FMCG baseline metrics (year-ended July 2025)

Implication: The sector’s immediate constraint was affordability and pack/format shifts — not absence of preference or long-term structural demand. That meant policy or price relief could trigger a sustained response if executed visibly.

II. The policy pivot that changed the game: GST 2.0

What changed

The government implemented a GST rationalisation effective 22 September 2025 which, for FMCG, broadly meant:

- Compression of multiple slabs; many mass-consumption items moved to 5% (from 12%/18%).

- Standard rate set at 18% and luxury/sin items moved to 40% to protect revenues.

- Legal notification and administrative guidance were issued ahead of implementation, causing short-term trade adjustments but giving market participants clarity.

Why it matters for FMCG

- Visible price reduction: A 5–10% effective cut on popular SKUs (depending on the product and trade margins) shifts the mental reference price consumers use — especially when savings accumulate across a primary shopping basket.

- Demand elasticity: Worldpanel’s analysis emphasised that main baskets (10–15 categories) are more sensitive to such cumulative savings — retailers and brands with presence in main baskets are positioned to benefit fastest.

- Trade & compliance simplicity: Fewer slabs reduce cascading effects, simplify invoicing and may lower compliance costs over time for manufacturers and distributors.

Short-term friction: The announcement and transition period led to trade channel disruption as retailers cleared old inventories or delayed orders to benefit from new prices — a drag that impacted Q2 numbers for several firms. But these disruptions were transient and expected to normalise.

III. The macro lever — disinflation restores purchasing power

The CPI easing in September 2025 to ~1.54% YoY (provisional) is the most consequential macro development since the Pulse baseline:

- Why it matters: Lower headline inflation immediately improves the real purchasing power of households. With food and edible-oil inflation easing, discretionary real consumption becomes plausible.

- How it interacts with GST: While GST lowers the tax component of price, disinflation improves the purchasing context — together they amplify perceived affordability and the propensity to spend.

- Investor & corporate reaction: Rating agencies and analysts flagged this combination (GST + low inflation) as net positive for consumption-led sectors and consumption-focused issuers.

IV. Q2 FY26 corporate reality: volume traction and margin pressure

Company filings and results for Q2 FY26 provide the clearest real-time evidence of how these forces played out. Below is an integrated snapshot and analysis.

Q2 FY26 snapshot: selected FMCG majors

Analysis — what the Q2 scoreboard tells us

- Top-line recovery is visible across the board. Several bellwether firms (HUL, Nestlé India, Marico) reported revenue improvements in Q2, reflecting renewed demand and an easing of price pressure psychology. HUL’s USG of 2% — while modest — is notable because it occurred amidst GST transition and seasonal monsoon variability, implying underlying resilience.

- Margins remain under pressure in the near term. Across the cohort, profit lines and EBITDA were mixed. Nestlé India’s revenue improvement yet sharp PAT decline underscores lingering commodity and operating cost effects. HUL reported EBITDA of 23.2% but with UVG (Underlying Volume Growth) flat — volume expansion will be the key to margin rebound.

- GST transition created short-term trade friction. Q2’s numbers are affected by the timing of the GST notification and implementation as retailers and distributors delayed orders and cleared old-MRP stocks — a phenomenon seen across Colgate, HUL and others. These are one-off transitional effects likely to normalise in H2.

- Premiumisation and portfolio differentiation continue. Marico’s strong revenue growth, driven by premium hair oils and value-added foods, and Dabur’s emphasis on health & OTC categories indicate that consumers are still trading up in selected categories even as they trade down in others. This divergence supports a strategy of graded premiumisation.

- Companies are explicitly optimistic about the medium term. HUL’s CEO Priya Nair highlighted that the GST change is expected to boost disposable income and unlock premiumisation opportunities; the company’s listed priorities (segmentation, brand modernisation, sales machine future-proofing) show a playbook that aligns with the structural shift toward volume-led recovery.

V. The festive effect — real-time barometer of demand

The GST reform landed just as India entered its major festival season — a timing that magnified the reform’s impact. Early indicators:

- E-commerce & quick commerce spikes: Online order volumes jumped significantly during the early festival weeks, with a disproportionate share coming from tier-II/III towns. This quick-commerce growth is particularly important for impulse and replenishment buys that help lift FMCG volumes.

- Retail uptick in key states: Brick-and-mortar retailers in consumer-heavy states reported double-digit jumps vs. same period last year, attributing part of the rise to visible price relief and pent-up demand.

- Auto & durable signals: Across discretionary consumption, small car bookings surged after GST benefits on small cars — a broader sign of improved affordability and consumer intent that can ripple into FMCG via replenishment cycles.

Implication: Festive uplift is acting as the accelerant — but the sustainability of the increase will depend on visibility of price cuts at point of sale and the speed with which the trade and supply chain stabilise post-GST.

VI. Consumer psychology and structural shifts — the demand engine

A sustainable recovery requires behavioural change, not just temporary stimulus. Key dynamics observed:

1. Multi-category basket economics

If the average main shopping basket (15 categories) shows visible savings of ₹150–₹200 per trip, the probability of incremental purchase or category addition increases materially. Brands central to main baskets (staples, cooking media, fabric care, and basic personal care) benefit most from this dynamic. Worldpanel’s research supports this.

2. Premiumisation coexists with value

Consumers are simultaneously trading up for health, convenience and premium experiences, and trading down in pack or brand in categories where costs bite. This split is an opportunity: brands that create clear “value-plus” propositions (e.g., fortified staples, health-tagged snacks, premium hair/skin formats with accessible pack sizes) can capture margin and volume.

3. Tier-II/III and rural as structural drivers

Consumption patterns indicate that tier-II/III homes buy more FMCG (kg/yr) and that rural markets are closing the gap rapidly. Penetration gains, a lower cost of living, and improved digital access make these geographies the primary battlefield for growth.

4. Convenience and speed formats gain share

Ready-to-cook, porridge/oats, small-pack snacks and quick meal options grew fastest in the Pulse baseline and continue to outperform, meeting urban and peri-urban time constraints while offering affordability.

VII. Channel evolution — omnichannel shapes winners

The channel environment is remaking how FMCG reaches consumers:

- General trade (kiranas) remains dominant by volume but is being rapidly bolstered by digital enablement (wholesale & micro-order apps, credit flow).

- Modern trade is growing footprint and basket size for premium and promotional buys.

- E-commerce and quick-commerce are no longer urban niches; their penetration in tier-II/III towns is rising, providing incremental reach and trialability.

- D2C and subscription models are relevant for niche, premium and functional products, allowing margin retention and direct consumer insights.

Strategic implication: Brands must harmonise pricing and availability across channels (price parity + visibility), invest in last-mile micro-logistics, and use digital data to tweak SKU/shelf strategies regionally.

VIII. Scenario modelling and the next 12–18 months

We construct a practical model to help stakeholders set expectations.

Three scenarios for FMCG volume growth (FY26)

- Cautious (3–4%) — delayed or partial pass-through; commodity spike; trade friction persists.

- Base (5–6%) — partial pass-through; stabilization of input costs; rural & quick-commerce growth consolidates.

- Optimistic (7–8%+) — full and visible pass-through; commodity softening; strong festival adoption; rural acceleration.

Probability & preferred planning: Most indicators point to the Base scenario as the most likely near-term outcome. However, if companies accelerate visible pass-through and the trade normalises quickly, the Optimistic scenario is feasible, especially for value and premium adjacent categories.

IX. Financial & margin dynamics — how profitability recovers

Profit rebound is conditional on several interlinked dynamics:

- Volume scale: higher throughput dilutes fixed costs and recoups promotional investments.

- Input cost normalisation: as commodity prices ease, gross margin restoration becomes possible. Nestlé’s Q2 margin squeeze is instructive: revenue growth did not translate to profit due to cost lags.

- Mix & premiumisation: higher share of premium SKUs elevates ASP (average selling price) and gross margins, as seen in Marico’s performance.

- Operational efficiency: firms focusing on automation, SKU rationalisation and supply-chain digitisation will protect margin recovery.

- Trade economics: judicious trade support (to help pass-through) rather than margin hoarding will create sustainable demand — and ultimately better margin through volume rather than retained tax benefits.

Conclusion: Profitability is likely to lag volumes but should recover meaningfully through H2 FY26 into FY27 if the base case plays out.

X. Strategic checklist for stakeholders (manufacturers, retailers, distributors, investors)

For manufacturers

- Communicate visible price reductions where applicable; prioritise categories central to main shopping baskets.

- Accelerate pack innovation: affordable premium, value bundles, and small packs.

- Invest in regional go-to-market and digital trade enablement (micro distributors).

- Hedge commodity risk and rationalise SKUs for working capital efficiency.

For retailers & distributors

- Leverage GST-driven price points in promotion calendars; align with farmer pay cycles and festivals.

- Implement fast inventory turnover to avoid pre-GST old-MRP stock issues.

- Use data-driven assortments for local demand; partner with brands on visibility.

For investors

- Look for firms with: diversified distribution, premium portfolio exposure, strong rural reach, and digital channel strength.

- Expect near-term margin variability as trade adjustments settle; focus on revenue resilience and structural gearing to growth.

XI. Closing narrative — what this means for India’s FMCG future

The picture that emerges from the baseline, the policy pivot, the macro relief and the corporate scoreboard is consistent and compelling:

- The demand engine is returning. Volume traction is visible across marquee players and is led by value and main-basket categories, improved rural income, and the digital channel’s expanding reach.

- Profitability is contingent on execution. Margins have not yet caught up to top-line recovery, but the path to recovery is clear: visible pass-through, input cost normalisation and mix shift toward premium/health skus.

- The structural shift favors adaptability. Firms that can orchestrate omnichannel parity, localised distribution, pack innovation and clear consumer communication will win share — not those that merely protect margins in the short term.

- Policymakers delivered a demand-side lever. GST 2.0 is a structural stimulus — not a cyclical rebate. If businesses and trade convert that into visible on-shelf benefits, consumption dynamics will lift sustainably.

Bottom line: FMCG has moved beyond the simple binary of ‘recovery’ or ‘slowdown’. It is entering a phase where demand elasticity, channel dynamics and strategic execution will determine winners. The probability is high that FY26 becomes a watershed year — not just a rebound but the start of a multi-year upcycle if stakeholders act decisively.

(Data inputs: Worldpanel by Numerator, Ministry of Finance/GST Council, MOSPI CPI, company filings – HUL, Nestlé India, Marico, Dabur, Godrej Consumer, Colgate, industry trackers and analyst reports)