As a Trillion-Dollar Grocery Consumption Wave Emerges, Why Quick Commerce Wins Convenience but Value Grocery Wins Scale

For the past three years, India’s grocery story has been dominated by speed. Ten-minute deliveries. Dark stores. Hyperlocal fulfilment. Instant gratification. From Bengaluru to Mumbai, consumers have embraced the convenience of ordering milk, bread, fruits or detergent and receiving them before a cup of tea has cooled. Quick commerce has become the defining narrative of Indian retail, attracting billions of dollars in investment and transforming consumer expectations.

Yet beneath the headlines lies a much larger story.

While quick commerce is reshaping shopping behaviour among affluent urban households, another retail model is quietly expanding across hundreds of cities and towns. Its promise is not speed but value. Its customers are not ordering emergency ice cream at midnight but stocking monthly grocery baskets. Its competitive advantage lies not in delivery time but in assortment, affordability and trust.

The future of Indian grocery retail may ultimately depend on which opportunity proves larger: the convenience needs of urban consumers or the value aspirations of hundreds of millions of emerging middle-income households. Recent research from Redseer, Bain & Company, NielsenIQ, Kantar, The Knowledge Company and industry data from FMCG companies suggests that the answer may surprise many observers. The next phase of grocery growth is likely to be driven not by faster deliveries, but by broader inclusion.

A Trillion-Dollar Consumption Wave Is Emerging

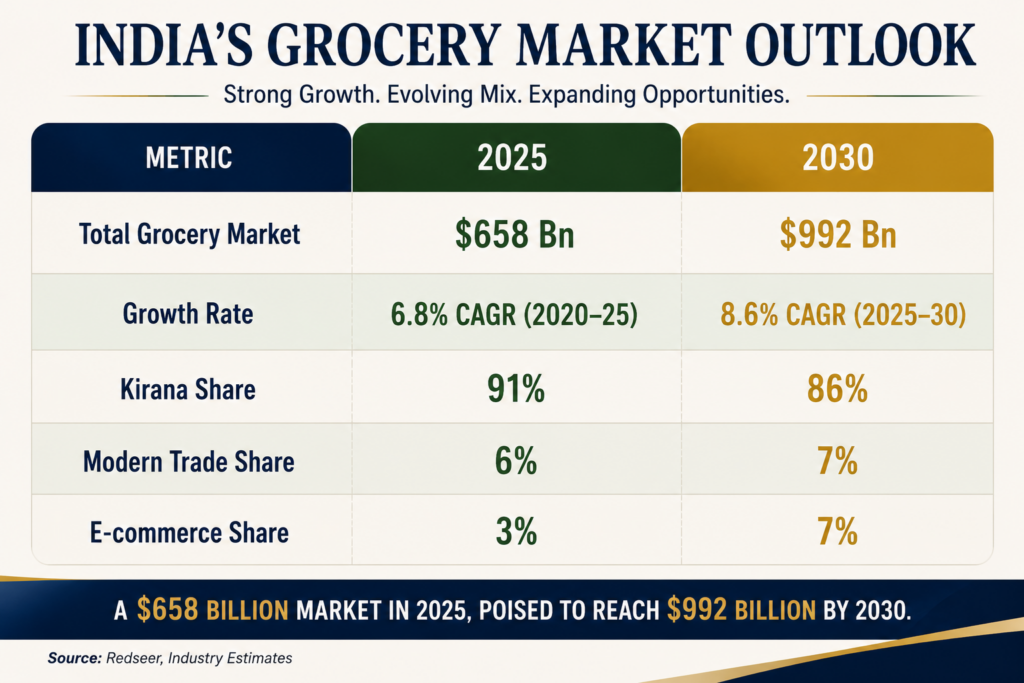

India’s grocery market is expected to expand from approximately $658 billion in 2025 to nearly $1 trillion by 2030, making it one of the largest food retail markets globally. At the same time, households earning between ₹3 lakh and ₹15 lakh annually are becoming the fastest-growing consumption segment. According to Redseer, consumption among emerging middle-income households could exceed $1 trillion annually by FY30, driven by more than 150 million households.

These consumers are not low-income shoppers.

Nor are they affluent metro households. They represent India’s largest and fastest-growing consumer cohort.

The Real Divide Is Not Geography

For years, grocery retail discussions have been framed as a contest between metropolitan India and smaller cities and towns. The reality is far more sophisticated. The fault line running through India’s grocery market today is not geographic but behavioural.

Increasingly, consumers are splitting into two distinct shopping missions.

The first is driven by convenience. These are the purchases made when milk runs out, when guests arrive unexpectedly, or when a family suddenly needs bread, eggs or snacks. Such purchases are typically small in value but high in urgency. Consumers prioritise speed over savings and are willing to pay a premium for convenience. This is the territory where quick commerce and hyperlocal delivery platforms thrive.

The second mission revolves around planned replenishment. These are weekly and monthly stock-up trips where households purchase staples, edible oils, packaged foods, personal care products and household essentials. Here, consumers are far more price-sensitive. They compare brands, seek discounts, explore regional options and optimise basket value. For these shoppers, assortment, affordability and reliability matter more than delivery speed.

This distinction is crucial because the economics of serving these two missions are fundamentally different. One rewards density and speed; the other rewards assortment depth, procurement efficiency and value engineering.

The Numbers Behind Quick Commerce

Few retail formats anywhere in the world have scaled as rapidly as quick commerce in India.

In just a few years, the sector has evolved from an experimental delivery model into a major retail channel. Industry estimates suggest that gross merchandise value (GMV) has nearly doubled from approximately $6-7 billion in FY24 to $13-14 billion in FY26. At the same time, quick commerce’s share of online grocery orders has risen from roughly half of all transactions to more than two-thirds.

The model has succeeded because it solves a genuine consumer problem. Urban households increasingly value time over money. For dual-income families, ordering groceries instantly often makes more sense than visiting a store.

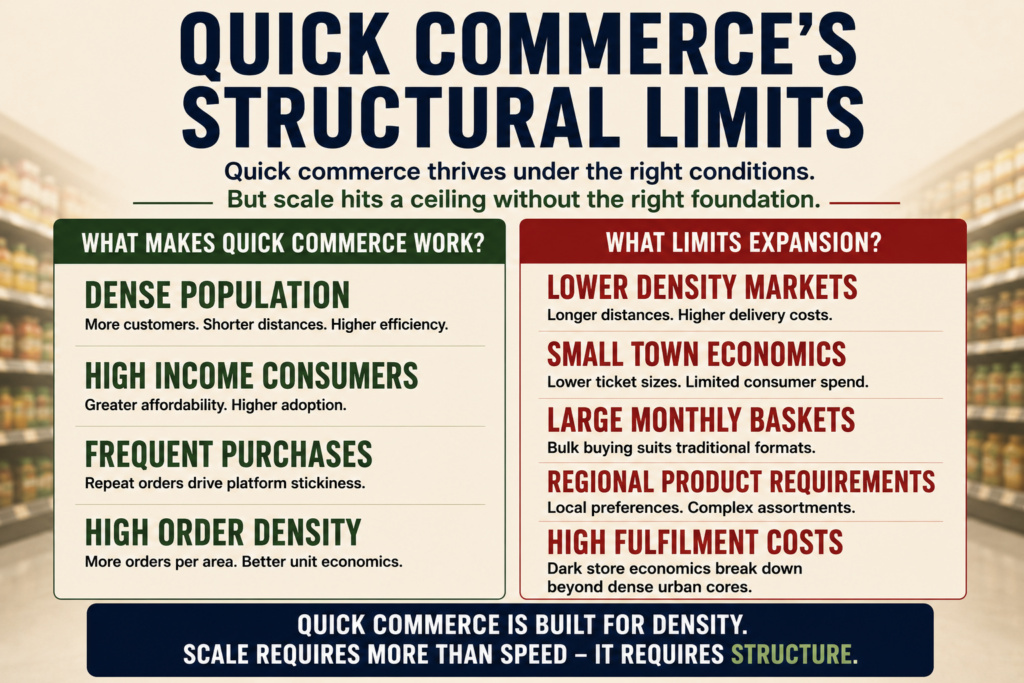

Why Quick Commerce Cannot Be The Entire Answer

Despite its growth, quick commerce faces structural limitations. Its economics depend heavily on population density. Dark stores become profitable only when a large number of consumers live within a small delivery radius. The model also requires significant investment in fulfilment infrastructure and inventory.

Assortment presents another challenge. Most quick commerce dark stores stock between 4,000 and 8,000 SKUs. By comparison, a large supermarket may carry 20,000 to 40,000 products. Most importantly, the model works best among consumers willing to pay a premium for convenience.

These factors explain why quick commerce remains heavily concentrated in major urban markets despite its impressive growth trajectory.

Why Value Grocery Is Gaining Attention

While investors have focused on speed, another model is quietly addressing a different consumer need. Value grocery platforms are designed around savings rather than immediacy. Instead of promising deliveries in ten minutes, they offer wider assortments, regional brands, affordable pack sizes and scheduled fulfilment. The objective is simple: help households optimise grocery expenditure.

This approach mirrors how a large proportion of Indian households actually shop. A family planning a monthly grocery basket is often more concerned about saving ₹50 on edible oil, finding a preferred regional atta brand or accessing trusted local snacks than receiving the order within minutes. In many ways, value grocery is attempting to digitise traditional grocery behaviour rather than reinvent it.

India’s Grocery Consumer Is Upgrading

Across FMCG earnings calls, consumer surveys and retail studies, one theme appears repeatedly: premiumisation. Indian households are steadily upgrading within categories. The shift is visible across staples, packaged foods, dairy and nutrition products.

Consumers who once purchased loose commodities are increasingly choosing branded alternatives. Functional benefits such as immunity, protein content and fortification are becoming mainstream purchase drivers.

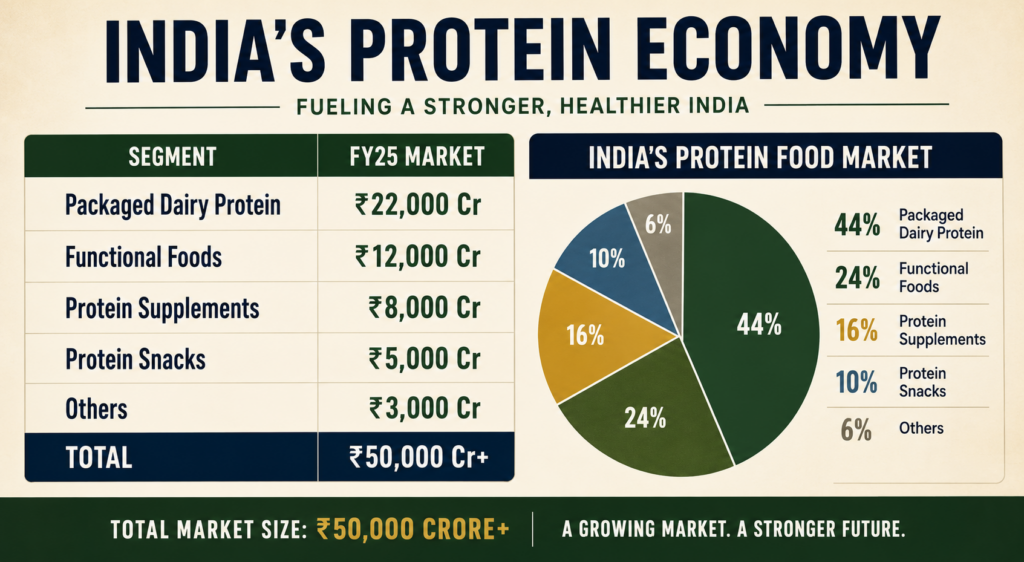

The Protein Revolution Reaches Mainstream Grocery

Perhaps the most significant shift underway is the emergence of protein as an everyday grocery category. Traditionally viewed as a specialised nutrition segment, protein is increasingly entering regular household consumption. Paneer, high-protein dairy products, protein snacks and fortified foods are moving from niche shelves into mainstream grocery baskets.

Industry estimates suggest India’s protein-focused food ecosystem already exceeds ₹50,000 crore.

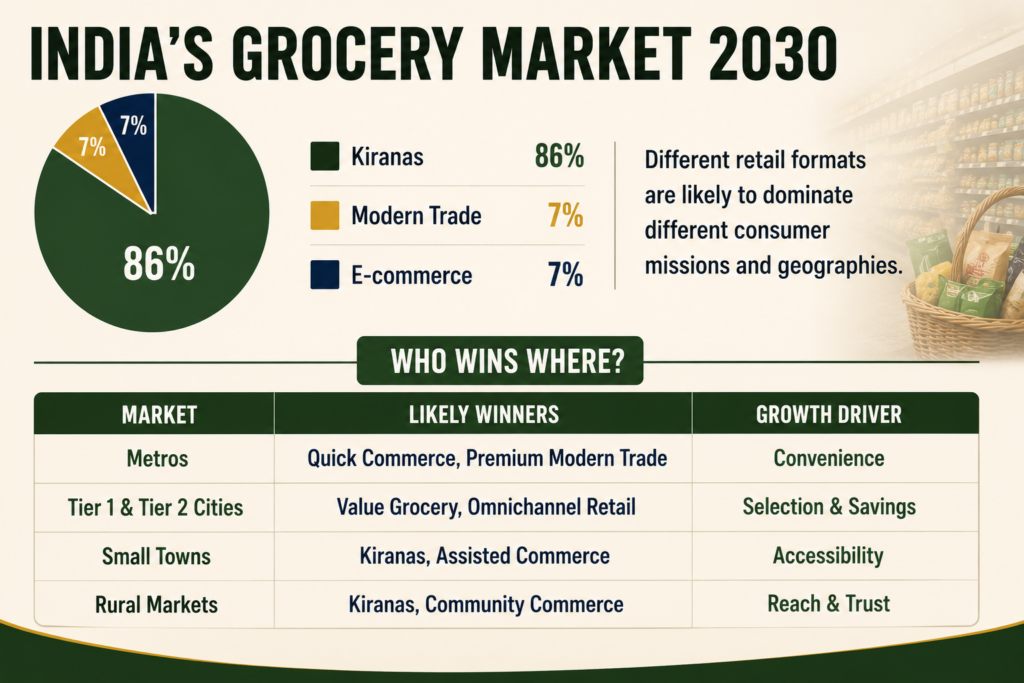

Why Kiranas Still Matter

Despite repeated predictions of disruption, kiranas remain the backbone of India’s grocery ecosystem. Even by 2030, they are expected to account for approximately 86% of grocery sales. Their resilience stems from advantages that are difficult to replicate digitally.

Trust built over decades, informal credit, proximity to households and deep understanding of local preferences continue to provide a powerful competitive moat. Far from disappearing, kiranas are increasingly becoming part of digital commerce ecosystems as fulfilment partners, pickup points and last-mile delivery enablers.

The Strategic Question

The future of grocery retail is unlikely to belong to a single format. Quick commerce will continue to expand, particularly in affluent urban markets. Modern trade will retain relevance in premium and experiential categories. Kiranas will remain deeply embedded in local communities.

The emerging opportunity lies in creating a profitable middle layer between traditional retail and convenience-led commerce. The most important grocery battle of the next decade may therefore not be Blinkit versus Zepto.

It may be whether organised retail can build a model that delivers affordability, assortment and trust to hundreds of millions of households that still conduct most of their grocery shopping offline.

If quick commerce represents the future of convenience, value grocery may well represent the future of scale. And in a market approaching one trillion dollars, scale is ultimately what determines long-term winners.